Credit is one of the important supply side factors which contributes to agriculture production. An effective credit delivery system is imperative for providing timely and adequate credit to the agriculture sector. Commercial banks, Regional Rural Banks (RRBs) and Co-operatives are the major financial institutions functioning in the area of finance. At the national level, during 2016-17, banks had disbursed 959,826 crore (provisional as on February 28, 2017) to the agriculture sector (including agriculture and allied, agri-infrastructure and ancillary activities), against a target of 900,000 crore, out of which commercial banks, RRBs and cooperative banks disbursed (provisional) 733,201 crore (76.3 per cent), 103,974 crore (10.8 per cent) and 122,651 crore (12.77 per cent) respectively. In 2015-16, the disbursement was 8.7 lakh crore. There has been an impressive growth in agricultural credit flow from 2.54 lakh crore to 9.60 lakh crore (provisional as on February 28, 2017) during the last ten-year period from 2007-08 to 2016-17. However, the share of term loan in the total agricultural credit disbursed declined steadily from 30.2 per cent in 2008-09 to 22.1 per cent in 2012-13, followed by a reverse trend, with the share of term loan touching 35.1 per cent in 2016-17.

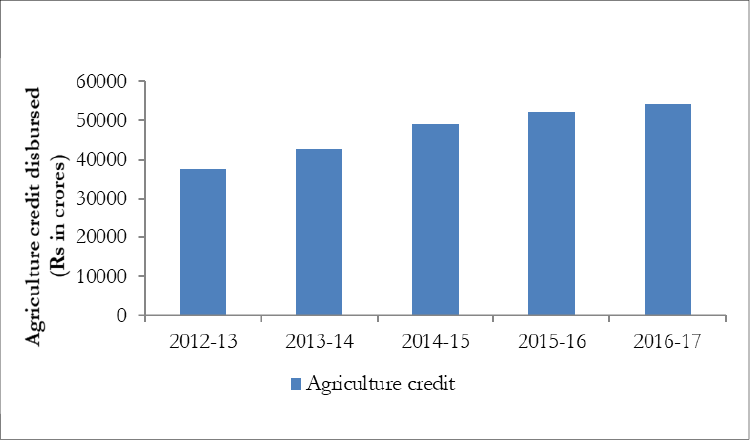

In Kerala too, agriculture advances has increased significantly in the last ten year period. The figures for the 12th Five-Year Plan period indicate that from 37,710 crore in 2012-13 it has increased to 54,270 crore in March 2017 showing a 43.9 per cent increase (Figure 2.3). As of now, it constitutes 5.64 per cent of the total agriculture advances in the country. Out of this, 33,802 crore (62.2 per cent) was disbursed by commercial banks, 8,515 crore (15.6 per cent) by RRB and 11,953 crore (22.2 per cent) by co-operative banks. Thus commercial banks continue to play a predominant role in the advance of credit in agriculture and allied activities

Source: SLBC

Source: SLBC

Investment Credit

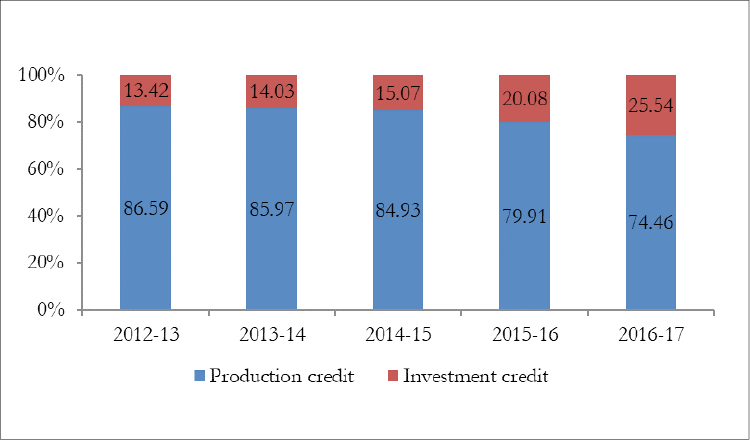

As regards the breakup of total agriculture credit to production and investment credit, it can be seen that the share of investment credit has increased to 25.54 per cent of the total credit from 13.4 per cent in the beginning of the 12th Plan period (Figure 2.4 and Appendix 2.23). This is definitely a positive development given the fact that share of investment credit had been consistently declining over the years from 22 per cent in 2008-09 to 11 per cent in 2011-12. However, the skewed ratio in favour of short term crop loan or production credit has resulted in low investment in capital/productivity enhancing assets. Hence, a segmentation approach could be adopted in credit delivery whereby the segment-/sector-specific credit requirements are assessed and differential rates of interest are enabled through subvention (keeping in view the net income per unit from a particular segment/sector/activity), to support activities that are critical but not picking up (State focus Paper, NABARD-2017-18).

Source: SLBC

Source: SLBC

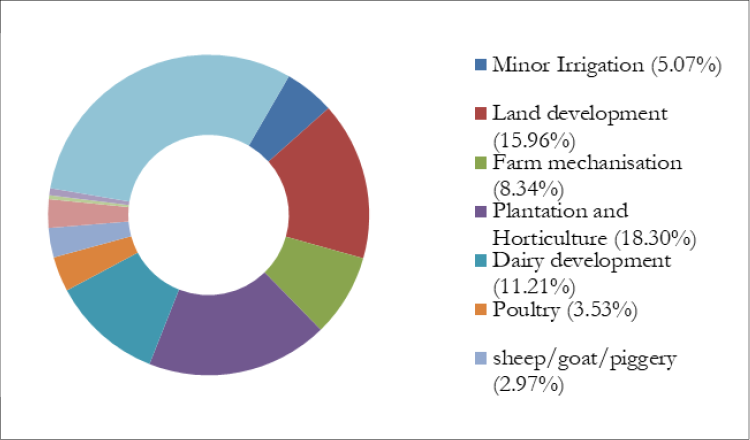

Analysis of the flow of investment credit to various subsectors revealed that in 2015-16, largest allocation was for plantation- horticulture (18.3 per cent) and land development (15.96 per cent). Farm mechanisation and dairy development accounted for 8.34 per cent and 11.21 per cent respectively. Productive sectors like fisheries, poultry, sheep goat and piggery accounted for less than 5 per cent (Figure 2.5 and Appendices 2.24 and 2.25).

Source: State Focus Paper 2017-18, NABARD

Source: State Focus Paper 2017-18, NABARD

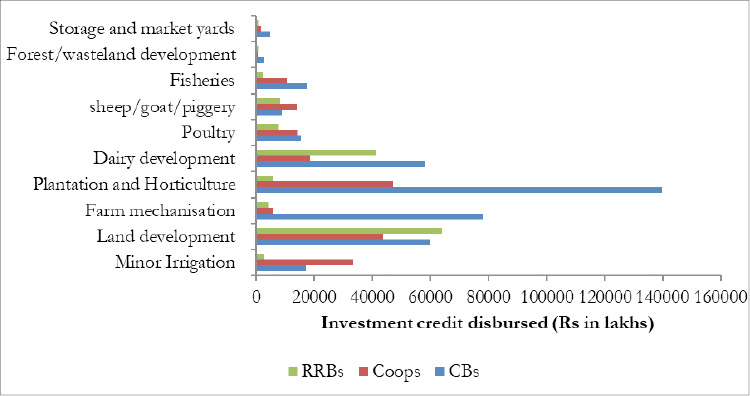

Agency wise flow of investment credit showed that commercial banks have disbursed the largest amount of credit (63 per cent) followed by co-operatives (22 per cent) and the rest by RRB. However, if we examine the area wise disbursement it can be seen that commercial banks have mainly focused on sectors like plantation and horticulture, farm mechanisation, land development and dairy development (Figure 2.6). Co-operatives on the other hand have focused on minor irrigation apart from plantations as well as land development while RRBs have given primary emphasis to land development and dairy development. Thus it can be inferred that the productive sectors like fisheries, sheep/goat/piggery and poultry development have been largely neglected from the point of view of investment credit.

Source: State Focus Paper 2017-18, NABARD

Source: State Focus Paper 2017-18, NABARD

Long Term Rural Credit Fund (LTRCF)

As the share of long term investment credit in agriculture is declining over the years, hampering the asset creation in agriculture activities and having an adverse effect on productivity in agriculture, Government of India has set up a “Long Term Rural Credit Fund” with NABARD for providing long term refinance support for investment credit in agriculture activities exclusively for cooperative banks and RRBs at a concessional rate of interest. All State Cooperative Banks, SCARDBs and RRBs which are eligible to avail refinance facilities from NABARD, subject to their satisfying the eligibility criteria, are eligible for LTRCF. Automatic refinance facility will be extended without any upper ceiling of refinance quantum, bank loan or total financial outlay for all projects under agriculture sector. 2015-16, Kerala had disbursed an amount of 750.00 crore to KSCARDB, 181.00 crore to KSCB and 38.00 crore to Kerala Gramin Bank under LTRCF.

Kissan Credit Card

Kissan Credit Card is an effective credit delivery tool for providing hassle-free timely and adequate credit. As per the reports available with SLBC, 518802 Kisan Credit Cards with an amount of 17826.27 crore have been issued during the 2015-16 in the State. As per the revised guidelines for KCC, the KCC should be a smart card cum debit card which could be used in the ATMs/hand held swipe machines etc. RuPay has come out with its RuPay KCC offering which leverages the benefits of both KCC and RuPay. Unlike normal KCC which serves only as an identity card and facilitates recording of transactions on an ongoing basis, RuPay KCC is actually a smart card that can be used at the nearest ATM/PoS for withdrawing cash. It removes the necessity of going to PACS or a bank branch to operate the account. At present issuance of RuPay KCC is on a pilot stage in Kerala.

Farmer Indebtedness in Kerala

The above analysis was about the disbursement of agriculture credit in the State. It is also important to know the composition of the loans from the point of view of a farmer or what is the level of farmer indebtedness in the State. The Situation Assessment Survey of Agriculture Households of the NSSO provides detailed estimates of the composition of outstanding loans in agriculture as well as the level of indebtedness in the country (Table 2.4). A perusal shows that, in Kerala, the total farm loans amount to 38,821 crore out of which 34,835 crore (89.7 per cent) is owed to formal institutions and a very a small percentage is sourced from informal ones. Also small and medium farmers account for a major share of the total formal loans. This is a pointer to the level of financial inclusion in the State, small and marginal farmers are not falling prey to the exorbitant rates charged by informal sources and moneylenders. This is in stark contrast to the overall picture of the country where as much as 85 per cent of the loans of small and medium farmers were sourced from informal sources.

| Small and Medium Farmers | Large Farmer | Grand Total | |||||||

| Formal | InformalInformal | Total | FormalFormal | Informal | Total | Formal | Informal | Total Total | |

| 34429 | 3993 | 38361 | 407 | 53 | 461 | 34835 | 3986 | 38821 | |

| 93253 | 208771 | 102024 | 31515 | 10645 | 42160 | 324768 | 219417 | 544185 | |

| Source: Economic survey 2016-17, GOI (Estimated from unit-level data on Situation Assessment Survey of Agriculture Households 2012-13 | 4075346134835398638821|||||||||

Assistance from NABARD

NABARD, Kerala disbursed financial assistance of 5820 crore in the State during the year 2015-16. Of the above, 5,090 crore was disbursed as refinance to banks, 600 crore to State Government under Rural Infrastructure Development Fund (RIDF), 115 crore as direct assistance to cooperative banks and 15 crore as grant assistance from dedicated funds to various agencies for various developmental and promotional activities. Out of the 5,090 crore disbursed as refinance, 2,390 crore was for long term investment credit and 2,700 crore was towards short term assistance to banks. The refinance for long term agriculture investment of cooperative banks was resumed in the current year after a gap of 10 years. Under RIDF, new projects worth 710 crore was sanctioned to State Government during the year.

RIDF

NABARD, since inception, has prioritised its strategies for facilitating credit flow to rural infrastructure sector to fulfill its mission of rural prosperity through credit and related services. From the year 1995 onwards, NABARD is funding rural infrastructure projects through its flagship programme of Rural Infrastructure Development Fund (RIDF) and as on date projects worth 2.602 lakh crore have been assisted throughout the country. In Kerala State projects with a total financial outlay of 9,789 crore involving RIDF loan of 8,172 crore have been assisted. In Kerala during the XXII tranche an amount of 673.99 crore was sanctioned and 134.80 crore was disbursed. The tranche wise sanction and disbursement under RIDF are shown in Appendices 2.26, 227 and 2.28.

Co-operation

Co-operatives in Kerala play a pivotal role especially in the rural area of the State owing to its huge network and unparalleled reach. They account for an estimated 21 per cent of the State’s total agricultural credit, have significant reserves, and often hand out money to fuel regional development. At a time when the country calls for inclusive growth as a key factor in removing socio-economic disparities, the cooperatives are the best organisation to achieve this objective as they are deeply rooted in the psyche of the people, are participatory by nature, and promote equity

At present there are 15,428 co-operative societies functioning under the Registrar of Co-operative Societies out of which 11,966 are working satisfactorily. Out of these majority are credit co-operatives (4,048) and consumer co-operatives (4,665) and 1,160 are women co-operatives. In addition, there are marketing, health and SC/ST co-operatives nearly half of which are either dormant or in loss. Details of the various types of co-operative societies are given in Appendices 2.29 and 2.30.

Credit Co-operatives

The credit co-operative societies are most vibrant and viable in the State. The co-operative credit structure in the State comprises short term credit and long term credit. The Short Term Agricultural Credit Structures mainly comprises the Kerala State Co-operative Bank (KSCB) at the apex level, 14 District Co-operative Bank (DCB) at the district level 1,647 Primary Agricultural Co-operative Societies (PACS) at the bottom level. These co-operatives are basically self-governing institutions with total accountability to the borrower members and in whose management they have a voice. In addition to the three-tire co-operative banking, there are well developed network of urban co-operative banks in the State.

In the long-term credit, Kerala State Co-operative Agriculture and Rural Development Bank (KSCARDB) is at the top and 78 Primary Co-operative Agricultural Rural Development Banks (PCARDB) at the bottom level. KSCARDB is playing an important role in promoting capital formation in agriculture and rural sectors in the State through its long term investment loans. The survival of KSCARDB and affiliated Primary Co-operative ARDBs in the long run depends on their ability to raise funds at reasonable cost that permits financing of farmers and other rural sections at affordable interest rates and to offer a complete range of credit and financial services to them.

The efficiency of the co-operative credit movement rests with the primary agriculture credit societies functioning at the grass root levels. There are 1,647 societies functioning in the State with a membership of 2.35 crore. However, during the period under review, the share capital of the societies has increased from 1,497.06 crore to 1,802.81 crore. The deposits during the year have increased from 80,190.41 crore to 83,157.38 crore while the loans issued has declined from 76,007.84 crore to 75,350.90 crore. Out of the total loans issued, the share of agriculture loans comes to around 10 percentage of the total loans issued. Also, one important development is the decrease in the medium term and long term loan for agriculture that will adversely affect capital formation. Selected indicators and credit operations of PACS are given in Appendices 2.31,2.32 and 2.33. During 2016-17, an amount of 34.25 lakh had been sanctioned to 35 PACS as share capital assistance.

Consumer Co-operatives

The overall aim of the consumer co-operative is to supply essential commodities at economic prices. These societies act as principal agents in the public distribution system by providing essential and consumer articles to the general public at a reasonable rate, than the rate prevailing in the open market. The organisational set up under the consumer co-operative segment consists of the Kerala State Cooperative Consumer Federation (apex) at the State level with 14 District Wholesale Stores and 643 Primary consumer stores at lower levels. The Kerala State Cooperative Consumer Federation (apex) makes bulk procurements and supplies these to District Wholesale stores, Department stores named Triveni and primary stores. The District whole sale stores and primary stores in turn cater to the needs of the consumer through their own outlets, super markets, and departmental stores.

Triveni super markets is one important segment under consumer co-operatives intending to save the public from the exploitation of middlemen by dealing with wholesale of food and grocery, cosmetics, household and electrical, textiles etc There are 204 Triveni Super markets in addition to mobile Triveni units and floating triveni super stores for supplying essential items to the public. The Neethi Scheme started as per directions of Government of Kerala in 1998 is being successfully implemented through 1,000 odd selected Primary Agricultural credit societies in all the districts of Kerala for the distribution of consumer goods at the lowest prices, especially in rural areas., Neethi medical stores were started for –providing medicines at subsidised rates. Consumerfed procures and distributes medicines at whole sale rates as per the requirement of the Neethi medical stores. At present there are 96 Neethi Medical Stores directly run by Federation in addition to the 600 odd stores run primary co-operative societies. Nanma stores was started to distribute 10 items of essential commodities at subsidised rates through network of 2180 retail outlets mainly aiming at the extremely poor and downtrodden in the society. Currently there are 751 Nanma stores run by the Consumer fed itself. 1,311 of them are run by selected co-operative societies and 869 by the Triveni wing of federation. Here the items are sold at less than 20 per cent of market rates. Another major project started is to open directly run Nanma stores in Panchayath and Municipal Wards having no Nanma stores run by primary societies at present.

Deposit Mobilisation Campaign by Co-operative Societies

Deposit Mobilisation campaigns by co-operative credit institutions continued during the year under report. During the period under review, the co-operatives could mobilise 6,386.18 crore as against the 7,311 crore in 2015-16. Year wise target and achievement is given in Appendix 2.34.

Achievements of the Sector in 2016-17

Formation of Kerala Bank

Government of Kerala has initiated the steps for forming the Kerala Bank by amalgamating the 14 District Co-operative Banks with branches across the State as well as the State Co-operative Bank into a single entity. With a large deposit base as well as holding a considerable share in the total banking transactions in Kerala, it is poised to become the second biggest bank- second to the State Bank Group. The cooperative sector was already wielding a considerable share of the banking business in the State and it could further grow, diversify, and fill the vacuum left by the State Bank of Travancore following its merger with the State Bank of India. The Kerala Bank and the PACS would function in a complementary manner. The PACS would continue their current banking operations and the Kerala Bank would focus on value-added services and specialised banking products.

Support by National Cooperative Development Corporation

National Co-operative Development Corporation or NCDC is a statutory organisation established by the Government of India under an Act of Parliament, charged with the function of planning and promoting programmes for the production, processing, marketing, storage, export and imports of agricultural produce and notified commodities and for distribution of agricultural production requisites through co-operatives. National Co-operative Development Corporation has emerged as a developmental and promotional financing institution for the co-operative sector in the country. NCDC (National Cooperative Development Corporation) has disbursed a cumulative financial assistance of 6736 crore for various cooperative development projects as on March 31, 2017, of which 1,610.84 crore is through State Government and 5,125.3 crore is via direct funding. Also, out of the 6,736.14 crore, 1,506.49 crore comes under long term loan and only 56.65 crore come under subsidy, 5, 173 crore comes under working capital. Types of NCDC Assistance are shown in Appendix 2.35.

In 2016-17, Kerala stood 6th in all India standing for disbursement of NCDC’s financial assistance to States. Sanctions and release of NCDC funds to the State of Kerala for 2016-17 was 603.73 crore and 462.79 crore respectively which comes to the tune of 2.39 per cent of the total sanctions and 2.91 per cent of the total releases made by the NCDC country wide. Cumulatively 108 cooperatives in Kerala were benefitted by NCDC funding through State Govt/Direct funding scheme during 2016-17 either through sanctions/disbursement of funds. Almost all sectors of Agriculture and allied activities including short term agriculture credit, marketing of agriculture produce, distribution of fertilizers and inputs, consumer cooperatives, Processing activities, storage/godowns, infrastructure creation, service sector, industrial cooperatives, Labour cooperatives and weaker section programme like fisheries, SC/ST etc. were covered by NCDC finance in the State during 2016-17. Details of NCDC assistance are given in Appendices 2.35, 2.36 and 2.37.