Aspects of international and domestic financial crisis have severe implications on the economy of State of Kerala. As is well known a sustained surge in demand is crucial to maintain sustained economic growth. Problems of external and domestic demand are thus important aspects of the recent problems of economic growth. Kerala State economy has historically been linked in different ways to the rest of the world and thus cannot be free from grave challenges of faltering economic growth in different parts of the world.

Policies of nationalisation implemented in the countries of the Gulf Co-operation Council have had an impact on the inflow of foreign remittances to Kerala and consequently on the household consumption demand. Other activities in the State, particularly, in the fields of trade, real estate, and construction are also weakened by any decline in foreign remittances. Performance in export oriented industries such as cashew, coir, handloom and in other cash crops assumes much significance in terms of economic output and employment in Kerala. A deceleration of export demand combined with national trade policies has resulted in a decline in the prices of plantation and related products, affecting adversely the traditional industries that have been the mainstay of State economy.

The State has always been proud of its high growth in State GDP with regard to the national average. However, the latest statistics of Central Statistical Organisation (CSO), State GDP growth are not very encouraging in this regard. The growth in the State economy now lags behind the national average for the first time. The growth of State Domestic Product, which consistently stood above the national average, began to show a declining trend from 2012-13 and further deteriorated to a level of 8.59 per cent in 2015-16, when the national average stood at the level of 9.94 per cent.

When the present government assumed office in 2016, it inherited a precarious legacy. The previous Government left behind a net unpaid negative treasury cash balance of 173.46 crore. The new government had to bear the brunt of huge magnitude of deferred liabilities of the previous government, amounting to around 6000 crore and also non-budgeted short term liabilities of 4300 crore. The new government had the difficult task of tiding over the huge financial burden shouldered upon it against the backdrop of low buoyancy in revenue receipts consequent on the previous governments’ imprudent taxation policies. The failure in tax administration is shown by the data of tax growth from 2010-11 to 2015-16. The tax growth which was at a high point of 23.24 per cent in 2010-11 declined sharply to the level of 10.68 per cent in 2015-16. The distress felt in State economy also led to low buoyancy in revenue growth. The government had to take strenuous fiscal correction measures to bring back State finances into a safer zone by means of improved tax collection by ensuring better compliance and implementation of technological improvement and efficiency in tax administration.

To overcome the stark economic problems of the day, the new Government took the bold step of presenting an alternative development model. In 2016, the State Government introduced a multi-pronged development strategy that included an attempt to achieve sustainable infrastructure growth, and provided comprehensive social security packages to vulnerable sections of the society. A package was also formulated to combat recession and economic stagnation. State Government infused substantial sums into the traditional sectors in order to rejuvenate industries such as cashew, coir, and handloom, where the livelihoods of thousands had been hit by sharp declines in commodity prices.

The macroeconomic problems of States were exacerbated by the demonetisation policy. As the report of the Committee on the impact of demonetisation on Kerala’s economy appointed by State Planning Board pointed out, purchasing power and economic activity in the State was severely affected by demonetisation.

Economic activities in sectors such as coir, handloom, agriculture and allied activities came almost to a standstill because of currency shortages. The co-operative sector, which has a long history in the upliftment of Kerala’s rural and urban economy, was brought to the verge of shutdown in the aftermath of demonetisation. The people had to undergo much hardship in the immediate post-demonetisation phase. Consumption demand stagnated. Investment was affected and a decline in economic growth was an inevitable consequence of demonetisation. Demonetisation led to a fall in GSDP and revenues. The revenue led fiscal consolidation policy was severely affected by unexpected policy of demonetisation. Increasing demand reflected in consumption expenditure is the mainstay of State revenues. Once consumption expenditure decelerates, so do inflows into State coffers. The fiscal cost of demonetisation was felt in its negative impact on the fiscal correction road map. The efforts of the State Government to raise tax revenues in 2016-17 was severely affected and the State was able to achieve 8.16 per cent growth against the revised targeted growth of 14.24 per cent, thus upsetting severely fiscal parameters envisaged in the Budget. The financial indicators for the State are given in Table 1.6.

| Particulars | 2010-11 | 2011-12 | 2012-13 | 2013-14 | 2014-15 | 2015-16 | 2016-17 |

| Balance from current Revenue (BCR) | -910 | -5449 | -4973 | -6917 | -9533 | -1322 | -5253 |

| Interest Ratio | 0.18 | 0.17 | 0.16 | 0.17 | 0.17 | 0.16 | 0.16 |

| Capital Outlay/Capital receipts | 0.43 | 0.31 | 0.29 | 0.25 | 0.23 | 0.42 | 0.38 |

| Return of Investment ratio | 0.020 | 0.016 | 0.016 | 0.018 | 0.012 | 0.013 | 0.013 |

| Outstanding Guarantees (including interest)/Revenue Receipts | 0.24 | 0.22 | 0.22 | 0.20 | 0.19 | 0.18 | 0.21 |

| Assets/Liabilities | 0.40 | 0.40 | 0.40 | NA | NA | NA | NA |

| Source: Finance Department, GOK. NA: Not availabl |

|||||||

The revenue-led fiscal consolidation strategy adopted by the State after enactment of Kerala Fiscal Responsibility Act 2003 had made significant strides in the State’s fiscal performance for a certain period of time. The revenue deficit which was 3.51 per cent of GSDP in 2002-03, came down to 1.13 per cent in 2010-11 and fiscal deficit decreased to 2.38 per cent from 4.24 per cent during this period. However after this period buoyancy in revenue mobilisation was not enough to sustain the fiscal performance that had been achieved. Revenue deficit and fiscal deficit ratio to GSDP during the period from 2011-12 to 2015-16 was in the range of 2.2 to 1.73 per cent and 3.52 to 3.19 per cent respectively. Revenue deficit and fiscal deficit ratio to GSDP could be sustained at this level during 2015-16, obviously because of fact that Central Government had awarded the post devolution revenue deficit grant of 4640 crore. However the fiscal indicators suffered a setback during 2016-17 due to certain explicit reasons. The proportion of revenue and fiscal deficit fell down to the level of 2.51 and 4.29 per cent of GSDP. The unexpected currency scrapping exercise had hit hard revenue buoyancy of the State in an unprecedented manner. Additional outgo consequent on implementation of 10th pay revision, clearance of huge amount of contingent liabilities left over by the previous government, disbursement of social security pensions with long pending arrears were also the major reasons behind slippage in fiscal indicators during 2016-17. Despite these facts it is noteworthy to point out that expenditure under health and education sectors had made sustainable increase of 26 per cent and 19 per cent respectively during 2016-17, which was a significant achievement in the midst of fiscal imbroglio. Major deficit indicators of the State for the period from 2010-11 to 2017-18 (BE) is shown in Table 1.7.

| Year | Revenue Deficit | Fiscal Deficit | Primary Deficit (-) /Surplus(+) | GSDP | |||

| Amount | % to GSDP | Amount | % to GSDP | Amount | % to GSDP | ||

| 2010-11 | 3,673.87 | 1.13 | 7,730.46 | 2.38 | -2,040.80 | -0.63 | 324,512.65 |

| 2011-12 | 8,034.26 | 2.21 | 12,814.77 | 3.52 | -6,521.17 | -1.79 | 364,047.88 |

| 2012-13 | 9,351.45 | 2.27 | 15,002.47 | 3.64 | 7,797.66 | 1.89 | 412,313.00 |

| 2013-14 | 11,308.56 | 2.43 | 16,944.13 | 3.64 | 8,678.74 | 1.87 | 465,041.21 |

| 2014-15 | 13,795.96 | 2.69 | 18,641.72 | 3.64 | 8,872.13 | 1.73 | 512,564.05 |

| 2015-16 | 9,656.81 | 1.73 | 17,818.46 | 3.19 | 6,707.61 | 1.20 | 557,946.51 |

| 2016-17 | 15,484.59 | 2.51 | 26,448.35 | 4.29 | 14,331.85 | 2.32 | 617,034.66 |

| 2017-18 (BE) | 16,043.14 | 2.14 | 25,756.32 | 3.44 | 12,124.49 | 1.62 | 747,945.00 |

| Source: Finance Department, GOK | |||||||

Receipts

State government receipts can broadly be divided into Revenue and Capital receipts. The revenue receipts comprise State’s own tax and non-tax revenues, share of central tax transfers and grants-in-aid from Government of India, whereas capital receipts mostly consist of disinvestment receipts, recoveries of loans and advances, debt receipts from internal resources and loans and advances from Government of India and net accretions under public account.

Revenue Receipts

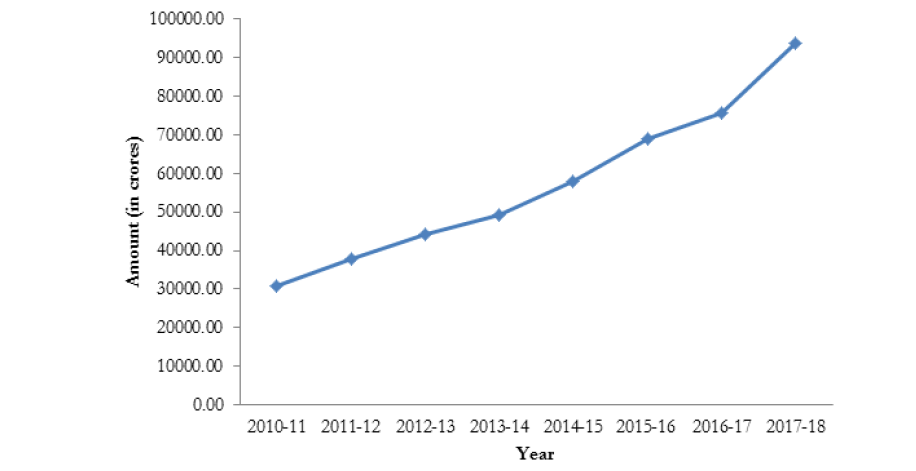

The revenue receipts of the State increased from 30,990.95 crore in 2010-11 to 75,611.72 crore in 2016-17. However during this period, growth rate of revenue receipts decreased from 18.70 per cent to 9.53 per cent. Revenue receipts of the State in proportion to GSDP decreased marginally to 12.25 per cent in 2016-17 from 12.37 per cent in 2015-16. The trend in Revenue Receipts from 2010-11 to 2017-18 (BE) is given in Figure 1.6.

State’s own taxes are the main source of revenue receipts of the State. In 2016-17, contribution from State’s own taxes was 42176.38 crore which constitutes 55.78 per cent of the total revenue collection. During this period, contributions from the share of central taxes and grants was 23735.36 crore and State’s own non-tax revenue was 9699.98 crore. The details of Revenue Receipts from 2010-11 to 2017-18 BE is given in Appendix 1.22

State’s Own Tax Revenue (SOTR)

The main sources of State’s Own Tax Revenue (SOTR) are Sales Tax including VAT, Stamps and Registration fees, State Excise Duties, Motor Vehicle Tax and Land Revenue. Growth rate of State’s Own Tax Revenue showed a declining trend for the last five years. In 2010-11, it was 23.24 per cent where as in 2016-17 it came down to 8.16 per cent. But the receipt from State’s Own Tax Revenue showed a marginal increase in 2016-17 (42,176.38 crore) against 2015-16 (38,995.15 crore). Of the SOTR, the major share was from sales tax including VAT. In 2016-17, receipts from sales tax and VAT contributed 33,453.49 crore which was 79.32 per cent of the total SOTR, followed by 7.37 per cent from taxes on vehicles (3,107.23 crore), 7.13 per cent from stamp duties and registration fees (3,006.59 crore), 4.79 per cent from State Excise Duties (2,019.30 crore) and 0.29 per cent from Land Revenue (124.15 crore). The receipts from Sales tax including VAT showed 8.84 per cent growth in 2016-17 over the previous year. The details of State’s Own Tax Revenue from 2010-11 to 2017-18 (BE) is given in Appendix 1.23.

State’s Own Non-Tax Revenue(SONTR)

Receipts under State Lotteries have been the major source of non-tax revenue of the State for last five years. Other main sources of SONTR are receipts from interest receipts and dividends, receipts from various social developmental services and sale proceeds of forest produces.

Receipts from SONTR showed an increasing trend for the last few years. But the annual growth rate of SONTR indicated a downward trend from 2013-14 onwards. In 2013-14, annual growth rate of SONTR was 32.79 per cent which became less than half in 2016-17 (15.13 per cent). In 2016-17, receipts from state lotteries were 7,283.29 crore recording a growth rate of 16.13 per cent compared to 2015-16 (6,271.41 crore). This constitutes 75.09 per cent of the total non-tax revenue of the State. The details of State’s own non-tax revenue from 2010-11 to 2017-18 (BE) is given in Appendix 1.24.

Central Transfers

Central transfers comprises of share in central taxes and grants in aid from Centre. State’s share in central taxes and grant in aid is determined on the basis of recommendations of the Finance Commissions. As per the recommendations of 14th Finance Commission, the share of the States on the net proceeds of Union Government during the period from 2015-16 to 2019-20 will be 42 per cent. The share pattern for the last two Finance Commissions viz. Twelfth (period 2005-10) and Thirteenth (period 2010-15) were 30.5 per cent and 32 per cent respectively. The State specific share during the 14th Finance Commission period is 2.5 per cent, as against the 2.36 per cent in the 13th Finance Commission award period.

The 14th Finance Commission has recommended 9,519 crore to the State for the period from 2015-16 to 2017-18 as Post Devolution Revenue Deficit Grant. Accordingly State had received deficit grant of 4,640 crore in 2015-16 and 3,350 crore in 2016-17. The receipt in 2017-18 would be 1,529 crore.

The annual growth rate of central transfers has increased from 2013-14 to 2015-16. The central transfers by way of share of central taxes and grant-in aid received in 2015-16 was 21,612.02 crore against 11,606.89 crore in 2013-14. But in 2016-17, even though the total central transfers increased, the annual growth rate decreased over 2015-16. In 2016-17, total Central transfers to the State was 23,735.37 crore against 21,612.02 crore in 2015-16. In this period share of central taxes was 15,225.02 crore witnessing a growth rate of 19.97 per cent. In 2016-17, the State had received 8,510.35 crore as grant in aid from Centre which includes Post Devolution Revenue Deficit grant of 3,350 crore. The details of central transfers from 2010-11 to 2017-18 (BE) is given in Table 1.8.

| Year | Share in Central Taxes and Duties | Grant-in-aid and other receipts from Centre for Plan and Non-Plan | Total Transfers | |||

| Amount | Annual Growth Rate (%) |

Amount | Annual Growth Rate (%) |

Amount | Annual Growth Rate (%) |

|

| 2010-11 | 5,141.85 | 16.89 | 2,196.62 | -1.65 | 7,338.47 | 10.65 |

| 2011-12 | 5,990.36 | 16.50 | 3,709.22 | 68.86 | 9,699.58 | 32.17 |

| 2012-13 | 6,840.65 | 14.19 | 3,021.53 | -18.54 | 9,862.18 | 1.68 |

| 2013-14 | 7,468.68 | 9.18 | 4,138.21 | 36.96 | 11,606.89 | 17.69 |

| 2014-15 | 7,926.29 | 6.13 | 7,507.99 | 81.43 | 15,434.28 | 32.98 |

| 2015-16 | 12,690.67 | 60.11 | 8,921.35 | 18.82 | 21,612.02 | 40.03 |

| 2016-17 | 15,225.02 | 19.97 | 8,510.35 | -4.61 | 23,735.37 | 9.82 |

| 2017-18 (BE) | 16,891.75 | 10.95 | 11,243.71 | 32.12 | 28,135.46 | 18.54 |

| Source: Finance Department, GOK. | ||||||

Expenditure

Expenditure of the State includes three components viz. revenue expenditure, capital expenditure and expenditure on loan disbursements. The total expenditure including Plan and non-Plan of the State is almost three fold from 2010-11 to 2016-17. The revenue expenditure as well as the capital expenditure was more than doubled during the same period. Out of the total expenditure of 102,382.55 crore in 2016-17, Plan expenditure was 22,812.61 crore (22.28 per cent) and non-Plan expenditure was 79,569.94 crore (77.72 per cent).

Revenue Expenditure

The revenue expenditure of the State is mainly comprise expenditure on salaries, pension, debt charges, devolutions to the Local Self Government and subsidies. The operational and maintenance cost for the upkeep of the completed projects and programmes are classified under the revenue account. Grants provided by the State to meet salaries and pension liabilities of employees in the Universities and state autonomous bodies and also the pension liabilities of employees of Panchayat Raj Institutions are classified under revenue expenditure. Major portion of revenue expenditure devolved to LSGIs utilised for the creation of capital assets at local body level.

Expenditure on social and economic services together constitutes developmental expenditure. Funds devolved to Local Self Governments for expansion and development and maintenance of assets is also reckoned as developmental expenditure. Non-developmental expenditure of the State mainly constitutes the committed expenditure consisting of debt charges, expenditure on pension payments and administrative services.

Annual growth rate of revenue expenditure has increased by 15.77 per cent in 2016-17 as against 9.68 per cent in 2015-16. The main reason for the hike in revenue expenditure during this period was the implementation of 10th pay revision. Distribution of social security pensions along with long pending arrears was another reason for increased revenue expenditure. Other factors that contributed for higher revenue expenditure are government’s market intervention activities to contain rise in prices of essential commodities and also due to government’s priority to impart quality services in health and education sectors. Total revenue expenditure in 2016-17 was 91,096.31 crore, of which Plan expenditure was 13,491.72 crore and non-Plan expenditure was 77,604.59 crore. The ratio of revenue expenditure relative to GSDP had shown a marginal increase of 14.76 per cent in 2016-17 compared to 14.10 per cent in 2015-16. The trend in revenue expenditure of the State from 2010-11 to 2017-18 (BE) is given in Figure 1.7 and more details including annual growth rate are given in Appendix 1.25.

The share of committed expenditure on revenue expenditure was increased during 2016-17 compared to the previous year. Expenditure on committed liabilities on salaries, pension, interest payments, subsidies and devolution to LSGs constitutes 69.31 per cent of revenue expenditure. In 2016-17, salary expenditure as portion of total revenue expenditure was 30.69 per cent where as it was 29.80 per cent in 2015-16. Pension expenditure as per cent of total revenue expenditure was 16.77 per cent in 2016-17 compared to 16.60 per cent in 2015-16. Interest payment as per cent of total revenue expenditure decreased to 13.30 per cent in 2016-17 from 14.12 per cent in 2015-16. Details on share of committed expenditure on revenue expenditure are given in Table 1.9 and details of developmental and non- developmental expenditure for the period from 2010-11 to

2017-18 BE are given in Appendix 1.26.

| Items | 2012-13 | 2013-14 | 2014-15 | 2015-16 | 2016-17 | |||||

| Expenditure | As per cent of TRE |

Expenditure | As per cent of TRE |

Expenditure | As per cent of TRE |

Expenditure | As per cent of TRE |

Expenditure | As per cent of TRE |

|

| i. Salaries | 17257.41 | 32.26 | 19279.78 | 31.88 | 21343.66 | 29.75 | 23450.10 | 29.80 | 27955.81 | 30.69 |

| ii. Pension | 8866.89 | 16.58 | 9971.27 | 16.49 | 11252.67 | 15.68 | 13062.86 | 16.60 | 15277.03 | 16.77 |

| iii. Interest | 7204.81 | 13.47 | 8265.39 | 13.66 | 9769.59 | 13.62 | 11110.62 | 14.12 | 12116.50 | 13.30 |

| iv. Devolutions to LSGDs | 4739.33 | 8.86 | 5926.00 | 9.79 | 7453.00 | 10.39 | 5028.92 | 6.39 | 6060.00 | 6.65 |

| v. Subsidies | 1265.20 | 2.37 | 1251.77 | 2.07 | 1247.52 | 1.74 | 1343.09 | 1.71 | 1730.00 | 1.90 |

| Committed Expenditure total (i to v) |

39333.64 | 73.54 | 44694.21 | 73.89 | 51066.44 | 71.18 | 53995.59 | 68.62 | 63140.01 | 69.31 |

| Others | 14155.10 | 26.46 | 15791.29 | 26.11 | 20679.99 | 28.82 | 24693.88 | 31.38 | 27956.30 | 30.69 |

| Total | 53488.75 | 100 | 60485.50 | 100 | 71746.43 | 100 | 78689.47 | 100 | 91096.31 | 100 |

| Source: Finance Department, GOK. | ||||||||||

Capital Expenditure

Traditionally share of capital expenditure in total expenditure is low. Deficit in resources is the major impediment in infrastructure financing. Government has therefore adopted alternative policy for financing major infrastructural projects for the sustainable development of the State economy. Alternative development model initiated by the government have already begun to show positive signs in attracting long term investment in capital projects.

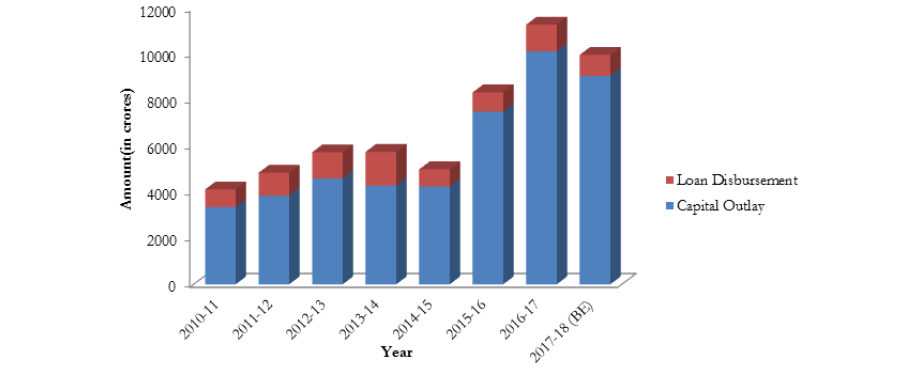

The share of government spending on capital projects in various sectors has increased during recent years. Substantial increase was noticed in capital outlay of the State during 2016-17, which increased to 10,125.95 crore from 7,500.04 crore in 2015-16. Capital outlay to GSDP ratio was also increased to 1.64 per cent in 2016-17 from 1.34 per cent in 2015-16. The public works continued to remain the major segment of capital outlay with 27.81 per cent of the total capital outlay in 2016-17 followed by irrigation (6.66 per cent), agriculture and allied activities (5.49 per cent) and industries (5.10 per cent). Details of capital expenditure from 2010-11 to 2017-18 (BE) are given in Appendix 1.27 and Appendix 1.28 and trend in capital outlay and loan disbursement are shown in Figure 1.8.

Debt Profile

Borrowings which are repayable and on which interest accrues are classified as debt. Debt of the State comprises of internal debt, loans and advances from Central Government and liabilities on account of Small Savings and Provident Fund Deposits, etc. During the last five years market borrowings and accretions in Small Savings and Provident Fund Deposits are the main source of the State Government to finance the fiscal deficit. Outstanding debt liabilities of the State at the end of 2016-17 were 186,453.68 crore. The annual growth rate of debt has increased to the level of 18.48 per cent in 2016-17 from 16.19 per cent in 2015-16. The Debt to GSDP ratio in 2010-11 was 24.24 per cent. In 2016-17, it stood at the level of 30.22 per cent. The ratio of debt in terms of revenue receipts increased to 246.59 per cent in 2016-17 from 227.97 per cent in 2015-16.

The share of internal debt in the total debt liabilities of the State comes to 63.43 per cent in 2016-17. Outstanding debt under internal debt increased to 118,268.72 crore in 2016-17 from 102,496.26 crore in 2015-16. The growth rate of internal debt in 2016-17 was 15.39 per cent. The liabilities under small savings, PF, etc. come to 32.49 per cent of the total liabilities. The liabilities under Small Savings, Provident Fund etc at the end of 2016-17 were 60,571.01 crore. The outstanding liabilities under Loans and Advances from the Centre at the end of 2016-17 were 7614.13 crore. The gross and net retention of debt in 2016-17 was 28,451.61 crore and 16,334.78 crore respectively. Details of debt profile of the State are given in Table 1.10 and details of receipts and disbursements are given in Appendix 1.29.

| Year | Internal Debt | Growth Rate (%) | Small Savings, Provident Fund, Others | Growth Rate (%) | Loans and advances from Central Govt. | Growth Rate (%) | Total | Growth Rate (%) |

| 2010-11 | 48,528.10 | 11.90 | 23,786.06 | 11.69 | 6,359.08 | 0.86 | 78,673.24 | 10.86 |

| 2011-12 | 55,397.39 | 14.16 | 27,625.10 | 16.14 | 6,395.69 | 0.58 | 89,418.18 | 13.66 |

| 2012-13 | 65,628.41 | 18.47 | 31,310.65 | 13.34 | 6,621.78 | 3.54 | 103,560.84 | 15.82 |

| 2013-14 | 76,804.35 | 17.03 | 35,542.51 | 13.52 | 6,662.21 | 0.61 | 119,009.07 | 14.92 |

| 2014-15 | 89,067.91 | 15.97 | 39,307.28 | 10.59 | 7,065.05 | 6.05 | 135,440.24 | 13.81 |

| 2015-16 | 102,496.26 | 15.08 | 47,639.36 | 21.20 | 7,234.71 | 2.40 | 157,370.33 | 16.19 |

| 2016-17 | 118,268.72 | 15.39 | 60,571.01 | 27.14 | 7,614.14 | 5.24 | 186,453.87 | 18.48 |

| 2017-18 (BE) | 139,646.01 | 18.08 | 58,318.02 | -3.72 | 9,062.78 | 19.03 | 207,026.81 | 11.03 |

| Source: Finance Department, GOK. | ||||||||

The introduction of GST is one of the landmark tax reforms in the post-independent history of India. It is widely presumed that introduction of GST would augment efficiency in economic activities and would benefit the State in the enhancement of indirect tax proceeds, once the technical glitches encountering in the initial phase of introduction of the new tax regime are cleared. The State Government have made laudable interventions in the GST councils time and again to bring in structural changes in the GST system and in the tax rates for getting maximum benefits to the State and also to protect the interest of the consumers. GST is a destination tax and Kerala is a consumer State. Kerala being a consumer State has every reason to hope that, GST would fetch more tax revenue for the State and achieve desired growth of more than 20 per cent in tax revenues in the years to come. Moreover, considering share of service sector in the State GDP, the benefit of GST to the State is expected to be more enormous. Once the current issues in GST system are resolved, State is optimistic about a positive turnaround in its revenue growth and revenue led fiscal consolidation can be restored sooner rather than later. However the implementation of GST has been beset with numerous problems particularly with regard to the IT backbone. Further numerous rate changes, failure to ensure that the benefits are passed on to the consumers, absence of e-way bill, changes in the threshold and even attempts to tinker with the architecture of GST have brought confusion and popular protest. The State Government has little power to intervene in this situation. Important fallout of GST has been the erosion of taxation powers of the State.

The State government has already succeeded in creating an ambience for attracting large scale investments in major infrastructure projects through innovative financial instruments like Alternative Investment Fund (AIF) Infrastructure Investment Trust (InvIT) and Infrastructure Debt Fund (IDF). For this purpose KIIFB acts as the key SPV for mobilising and channelising resources for various infrastructure SPVs. Genuine efforts are already on the part of government to create an image of Kerala being an investment friendly State. Apart from this, Govt. have launched four mission programmes – Life Mission, Haritha Keralam, Aardram and Comprehensive Educational Rejuvenation Programme – with people’s participation and by amalgamating various schemes under socio-economic development sectors. The alternative model adopted for development of infrastructure sector and mission mode programmes would prove to be the milestone for the multi-dimensional development of the State.

Contingent Liabilities

To overcome the ceiling on fiscal deficit set by the Fiscal Responsibility Act, the State Government is giving guarantees to the borrowings of public sector undertakings and other institutions instead of funding them directly through Budget. These contingent liabilities become the debt obligations of the State in the event of default by the borrowing public sector units for which Government is a guarantor. The outstanding guarantee in 2016-17 is 20,204.10 crore. The outstanding guarantees of the State Government from 2010-11 to 2016-17 are shown in Table 1.11.

| Year | Maximum amount Guaranteed |

Total Amount outstanding (including principal & interest) |

| 2010-11 | 12,625.07 |

7,425.79 |

| 2011-12 | 11,332.11 |

8,277.44 |

| 2012-13 | 11,482.25 |

9,099.50 |

| 2013-14 | 12,275.21 |

9,763.36 |

| 2014-15 | 13,123.30 |

11,126.67 |

| 2015-16 | 13,712.77 |

12,438.52 |

| 2016-17 | 20,204.10 |

16,245.55 |

| Source: Finance Department, GOK. | ||